Europe gas storage shortfall and TTF price outlook

June 25, 2026

Europe’s gas storage deficit: the real driver of TTF Win-26 upside

European gas prices sold off sharply in mid-June following the announcement of the

US–Iran memorandum of understanding. Markets moved quickly to price in a rapid resumption of Qatari LNG exports through the Strait of Hormuz and treated the diplomatic agreement as broadly resolving the risk to regional supply. We think that conclusion is premature and we expect a reversal to the TTF selloff once the market begins to reassess the pace of any reopening.

EU Storage (23 June 2026)

46%

50 bcm — of capacity

vs Same Point Last Year

−10.6 bcm

Year-on-year shortfall

vs Five-Year Average

−15 bcm

Below the five-year average

EA End-October Base Case

78%

85.8 bcm — neither figure is comfortable

The more important context for European gas prices over the coming winter is not the pace of Hormuz flows recovering but the state of its gas inventories by the start of the heating season. Europe entered the summer injection season in a significantly weaker position than in the last few years, and rebuilding stocks to an adequate level by 1 November will remain challenging even as Qatari supply recovers through Q3 26.

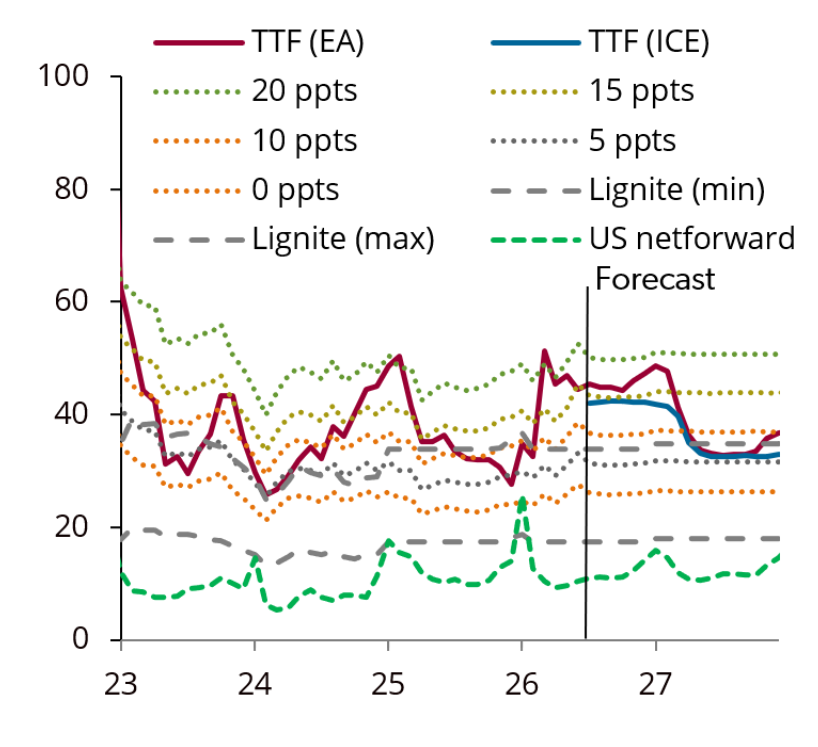

TTF vs coal–gas fuel-switch triggers, €/MWh

Source: ICE, ECB, Energy Aspects

Where European storage stands

EU storage stood at 50 bcm, equivalent to 46% of capacity, on 23 June. That is 10.6 bcm below the same point last year and 15 bcm below the five-year average. The shortfall has accumulated over a summer injection season constrained by a tight LNG market and a backwardated TTF forward curve — conditions that reduce the commercial incentive for active injection.

At the pace injections have been running, Europe would reach approximately 81.9 bcm (75% of capacity) by end-October. Our base case assumes a more active injection season from here, which we forecast lifts end-October storage to 85.8 bcm (78%). Neither figure is comfortable. End-October fill of 75–78% leaves limited headroom against a cold winter, particularly as storage withdrawal rates fall sharply once inventories drop below 50% of capacity.

10.6 bcm below last year; 15 bcm below five-year average

End-October projected at current rates

EA end-October 2026 forecast

German government end-October target — now on track via the seasonal contango

Germany’s situation is the most acute

Germany bears the greatest risk within this picture. The German government has a national storage target of 70% full by end-October. Germany is now on track to reach the target as THE seasonal spreads switch to a contango — but this does not resolve storage deliverability risks over winter.

Once storage falls below 50% of capacity, withdrawal rates drop sharply for physical reasons related to pressure and flow dynamics. For Germany, which sits at the centre of the Northwest European pipeline network, storage constraints translate quickly into deliverability risks for neighbouring markets. German supply stress in a cold spell does not stay within its own borders.

The government is reluctant to intervene directly through state-backed storage purchases. A more likely intermediate step would be instruments designed to make injection more economically viable. Given the scale of German injection demand, any such intervention would be a material price signal for TTF and THE prompt prices.

Why Qatari LNG will not close the gap quickly

Some of the bearish TTF move last week reflected expectations that Qatari LNG would resume quickly following the MoU announcement. We do not expect this. Hormuz traffic recovery will be gradual: mine clearance operations are under way but could take months, and the MoU assigns responsibility for this process to Iran. War-risk premiums remain elevated, P&I insurance terms require rewriting, and most vessel owners will want several weeks of incident-free transits before restoring pre-conflict deployment.

As Qatari exports resume on a gradual basis through Q3 26, initial volumes will be directed to intra-Gulf deliveries and Asian markets. European buyers are unlikely to see resumed Qatari deliveries before early Q4 26, at the earliest. Atlantic basin cargoes will continue to carry the weight of balancing the European market through the injection season.

19 June 2026

US–Iran MoU signed; TTF selloff

Q3 2026

Gradual Qatari LNG resumption; initial volumes to intra-Gulf and Asia

Early Q4 2026

Earliest realistic Qatari deliveries to Europe

This leaves TTF needing to price at a level that continues to attract flexible LNG cargoes away from Asian markets. Prices have partially corrected since Friday (19 June), unwinding some of the MoU-driven selloff, but price moves remain volatile amid bearish headlines. But the structural position of European storage means the case for TTF remaining elevated through Q3 26 is well-founded by the fundamentals, not merely by short-term sentiment.

The injection window is narrowing

The window for injection rates to accelerate is narrowing fast — European seasonal demand typically begins to pick up from late September, leaving little time for the storage deficit to close. The diplomatic progress following the MoU signing reduces the tail risk of an extended disruption to Hormuz flows, but it does not change the physical reality that European gas storage is running behind pace, that Qatari flows to Europe will return slowly, and that TTF prices need to be high enough to keep Atlantic cargoes flowing west.

We remain bullish on TTF near-curve contracts against the ICE forward curve.

The European gas balance over H2 2026 will be shaped by the pace of injection season recovery, the timing of Qatari LNG export recovery and the competition for cargoes between European and Asian buyers.

Our Europe Gas and Global LNG services track these dynamics in weekly detail, combining storage data, LNG flow analytics and fundamental price forecasting.

Recent Posts