Why shippers are unlikely to return quickly even after a deal

Most shipowners, refiners and traders view transit risks as too high, not only now but even in the early days after the strait reopens. The risk of sporadic attacks by Iran's proxies cannot be ruled out. Insurance premiums for Hormuz transits remain at levels that make many routes uneconomic. The central question is not whether isolated vessels can pass, but whether flows can resume at scale and with enough reliability to support genuine normalisation.

Several Gulf producers are developing or expanding pipeline routes that bypass Hormuz to reduce long-term exposure. This is a structural shift that will outlast the current conflict, underscoring that even market participants with direct stakes in Hormuz

do not expect a return to pre-conflict normality.

What does EA's proprietary geospatial data show about inventory pressure?

The stranded volumes within Hormuz have prevented Gulf producers from restarting upstream production or refineries that depend on export flows via the strait.

Kayrros satellite data show Iraqi onshore crude stocks have fallen by roughly 4 mb since mid-April as cargoes have been loaded from storage, but production is not yet being brought back online.

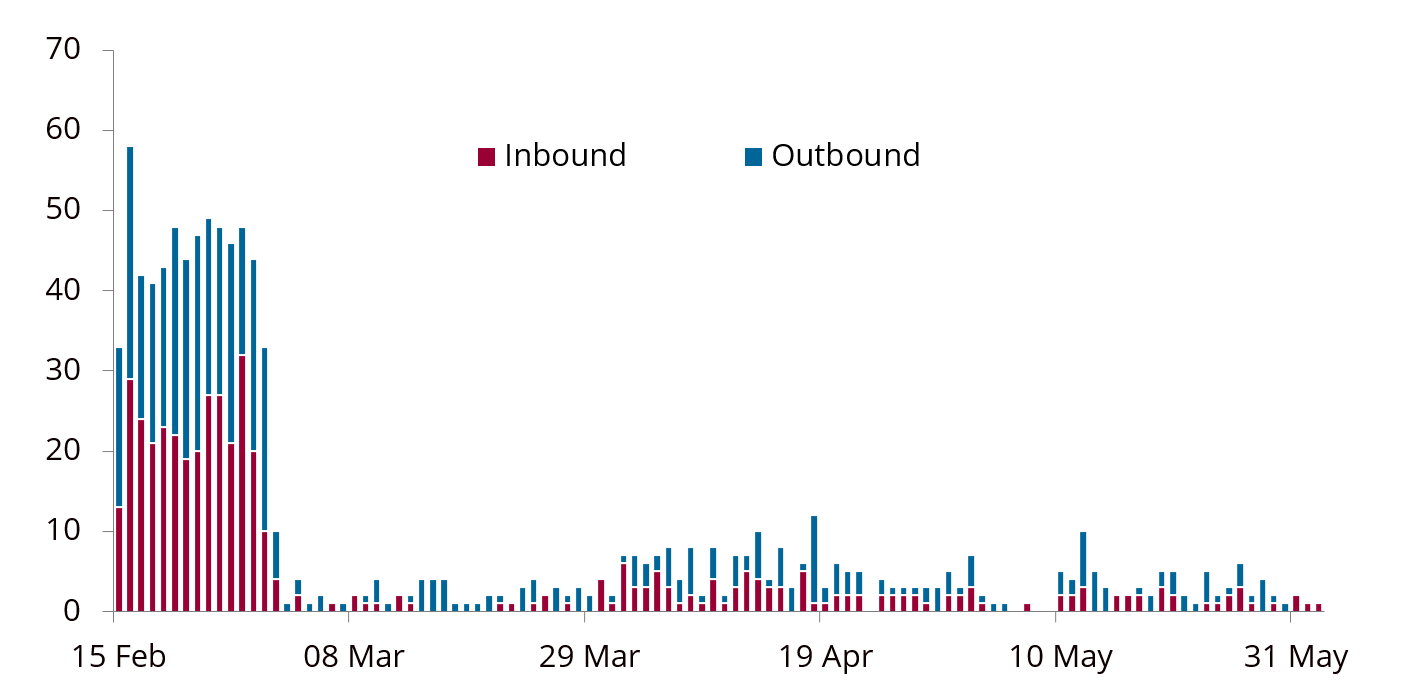

Meanwhile, the US blockade on Iranian exports has caused Iranian crude loadings to collapse to below 0.4 mb/d in May, from 1.8 mb/d in March. Crude tank utilisation at Kharg Island has risen to 84%, leaving only a few weeks before nationwide storage constraints begin to bite.

How should the market think about the recovery timeline?

We maintain our base case of oil transits reaching 50% of pre-war tonnage by end-June. Even this may prove optimistic. If disruptions extend into Q3 26, there are likely to be cascading supply shortfalls this summer, sharp price rises and medium-term impacts on global energy supply chains.

The largest disruption in oil and LNG market history is about to enter its fourth month. Government releases of strategic petroleum reserves have kept benchmark prices below demand-destruction levels for now, but the buffer is finite, the diplomatic path is uncertain and the operational challenges of restoring flows are substantial. A measured assessment of the recovery timeline requires looking beyond individual transits to the structural barriers that remain.