The product crisis building behind the crude headlines

April 27, 2026

Crude supply disruptions are dominating the narrative. But the tightness in refined products — jet fuel, diesel and gasoline — may prove more severe and longer-lasting. Here is what the market is underestimating.

Since the escalation of the Strait of Hormuz crisis, the energy market’s attention has been focussed on crude supply. That focus is understandable: upstream shut-ins across the Gulf have reached approximately 12 mb/d, while negotiations between US-Iran struggle to make progress, leaving markets to navigate headline risk.

But behind the crude story, a product crisis is building that could prove more consequential for consumers, refiners and policymakers — and it is not getting the attention it deserves.

The scale of the problem

The disruption to Middle Eastern refining capacity, combined with run cuts in Asia and now Europe, has removed an enormous volume of refined product from the global market. Energy Aspects estimates that over 450 million barrels of product output have been lost since the conflict began.

To put that in context: if demand remained unchanged and all other variables held constant, it would take until nearly 2030 to replace those lost barrels through normal refinery operations. That is not a realistic scenario — demand will adjust, as it always does — but it illustrates the depth of the deficit the market is facing.

Refinery run cuts globally are in the range of 5-6 mb/d. And unlike crude, where OPEC retains some limited spare production capacity, there is no equivalent buffer in the refining system. Global refineries were already operating at or near maximum utilisation before the crisis began.

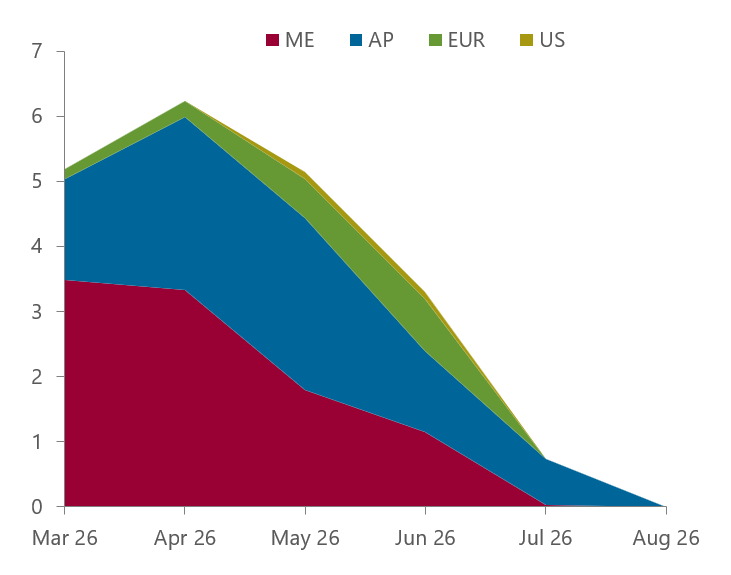

No refining capacity buffer

“Global refineries were already operating at or near maximum utilisation before the crisis began.”

Run cuts, mb/d

Source: Insights global, Energy Aspects

Which products are most exposed?

The impact varies by product, but the direction is uniformly tight.

Distillates have been hit hardest. The Middle East and Asia account for a large share of global diesel and gasoil exports. With run cuts concentrated in those regions and export restrictions now in place across several Asian countries, the flow of distillates to the rest of the world has slowed dramatically. European diesel stocks are well below five-year minimums and falling.

Jet fuel presents perhaps the most acute near-term risk. On a days-of-forward-cover basis, European jet stocks are critically low — in some markets, just weeks of supply remain. Energy Aspects expects stock-outs are possible later in the summer if the disruption persists. Some cancellations and flight route optimisation has already started across a number of major airlines as they brace for higher jet-fuel costs.

Gasoline has received less attention because it is not as directly exposed to Middle Eastern supply as diesel or jet. But the risk is building. Globally, the percentage of refineries incentivised to produce gasoline over jet and diesel has fallen to effectively zero. Refiners are maximising distillate and jet output because the economics overwhelmingly favour those products. That leaves gasoline as the residual — and with Asian buyers pulling European gasoline cargoes east, Atlantic basin gasoline tightness is emerging just as the Northern Hemisphere summer driving season approaches.

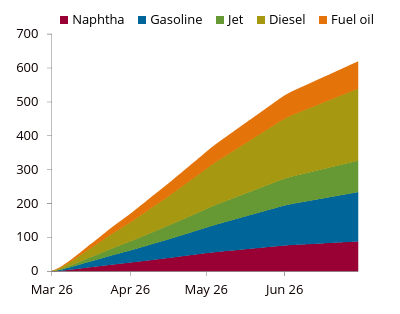

Iran conflict-related product supply loss, mb

Source: Argus Media Group, LSEG, Energy Aspects

Strategic petroleum reserves are masking the tightness

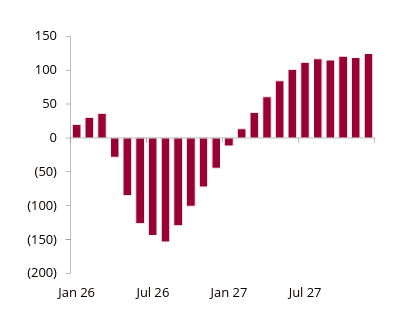

One reason the crisis has not yet triggered a sharper market reaction is that Strategic Petroleum Reserve (SPR) drawdowns, particularly in Asia, are bridging the gap. Japan is drawing strategic stocks at over 1 mb/d, and South Korea at around 0.3

In the West, the drawdowns have been more modest so far and led by the US. And that is precisely why the Western market has not yet felt the full severity of the product deficit. The SPR releases are a buffer, not a solution. They buy time, but they do not replace the lost refinery output. And every barrel drawn from strategic reserves today is a barrel that must be replenished later — adding to medium-term re-stocking demand.

Cumulative global liquids SPR change, mb

Source: OilX, Energy Aspects

The West has not felt the pinch yet — but it is coming

The timing of the product crisis is critical. Asian refiners are at their lowest point now — drawing on SPRs, cutting runs, and restricting exports to preserve domestic supply. The products they are not exporting would normally arrive in Western markets with a lead time of several weeks.

That means the full impact on European and US product markets is a May and June event. As the reduced Asian export volumes feed through, as European refinery run cuts deepen because of negative margins, and as SPR cover diminishes, the West will start to experience the tightness that Asia has been managing for weeks.

For jet fuel, the timeline is even tighter. European stocks have limited SPR coverage, and the summer travel season will test supply.

Prices must rise to curb demand

The disconnect between the severity of the product deficit and the relatively muted reaction in benchmark product prices cannot persist indefinitely. The crude market has done its work — physical crude prices have surged to levels that have destroyed refining margins and forced run cuts. The next leg of price adjustment must come from products.

Product prices need to rise to a level that achieves two things simultaneously: restoring refining margins so that the remaining operational capacity runs at maximum, and reducing demand enough to bring the market back into balance. Those are competing objectives — higher product prices improve margins but also accelerate demand destruction — and finding the equilibrium will be volatile.

What is clear is that the deferred portions of the product price curves — the months and quarters ahead — will have to roll up substantially from current levels. The market is not yet pricing the duration and depth of this product deficit, partly because the physical tightness has been concentrated in Asia and partly because SPR releases have obscured the underlying shortage.

The bottom line

The crude supply story is real and severe. But the product crisis may ultimately have a greater impact on consumers, on the political calculus around export restrictions and emergency measures. It is the part of this crisis that is still underpriced, and it deserves far more attention than it is getting.

This analysis draws on Energy Aspects’ latest webinar ‘Hormuz transit – exploring the new normal for energy markets, recorded 16 April 2026, featuring Dr Amrita Sen (Founder and Director of Market Intelligence), Richard Bronze (Head of Geopolitics) and Livia Gallarati (Head of Global Gas).

Recent Posts