EU ETS review: pragmatic Commission proposal softens LRF, introduces conditional free allocation, redesigns investment booster, and faces parliament amendments.

Global methanol demand growth slows to 1.2% in 2026 as the Iran conflict persists. We break down our long-term supply and demand outlook through 2030.

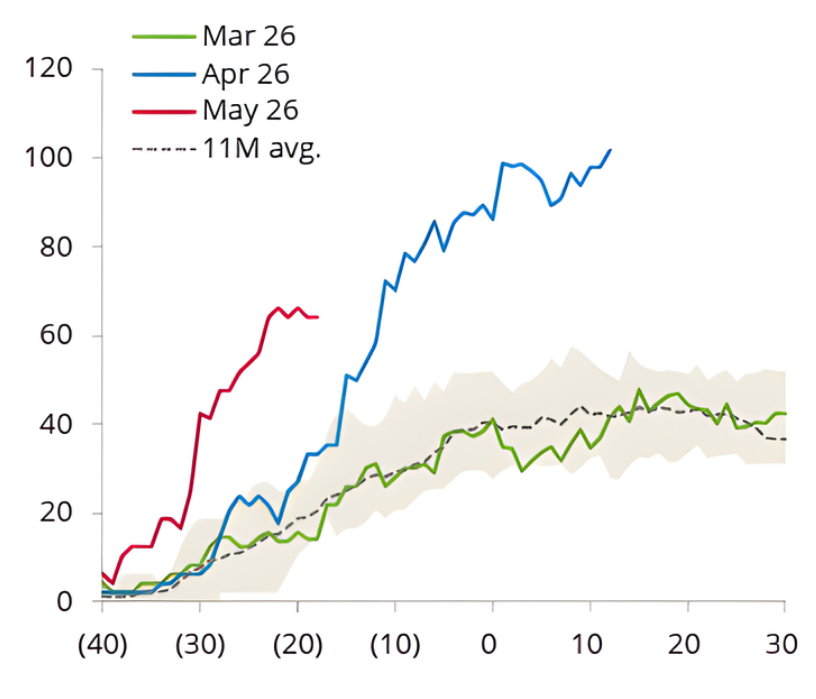

In energy markets, opinion is cheap. Data is cheaper. Learn how EA Analytics brings together what's happening, what it means, and what comes next.