What is happening to Middle Eastern methanol supply?

The US–Iran memorandum of understanding, signed in mid-June, briefly allowed a glut of stranded Middle Eastern methanol to reach China, India and other destinations, appearing to resume previous trade patterns. But we continue to expect considerable limitations in Middle Eastern supply until there is a lasting resolution to

Strait of Hormuz disruptions. Under this environment, non-integrated Chinese MTO units will idle or run at low rates, while CTO units continue operating at high, if somewhat reduced, rates as coal prices rise and demand softens approaching year-end. Middle Eastern methanol supply will remain constrained through Q3 26, and potentially longer, with all regional capacity and supporting infrastructure at risk of disruption until the Iran conflict is resolved.

How are demand trends shaping up in Europe and North America?

We have revised down our European methanol demand growth forecast, and now expect less than 1% y/y growth in 2026, as higher inflation and elevated energy and methanol costs weigh on consumption in the second half of the year. In North America, we still expect demand to increase moderately, particularly from derivatives used in domestic

oil and gas production. However, previous expectations of higher export demand for

acetic acid,

MTBE and biodiesel, where supply elsewhere is constrained by the Middle East conflict, have not fully materialised, due to production issues and limited demand for these products. Persistent inflationary pressure on raw material costs, including methanol itself, is also likely to limit North American demand growth in the second half of the year.

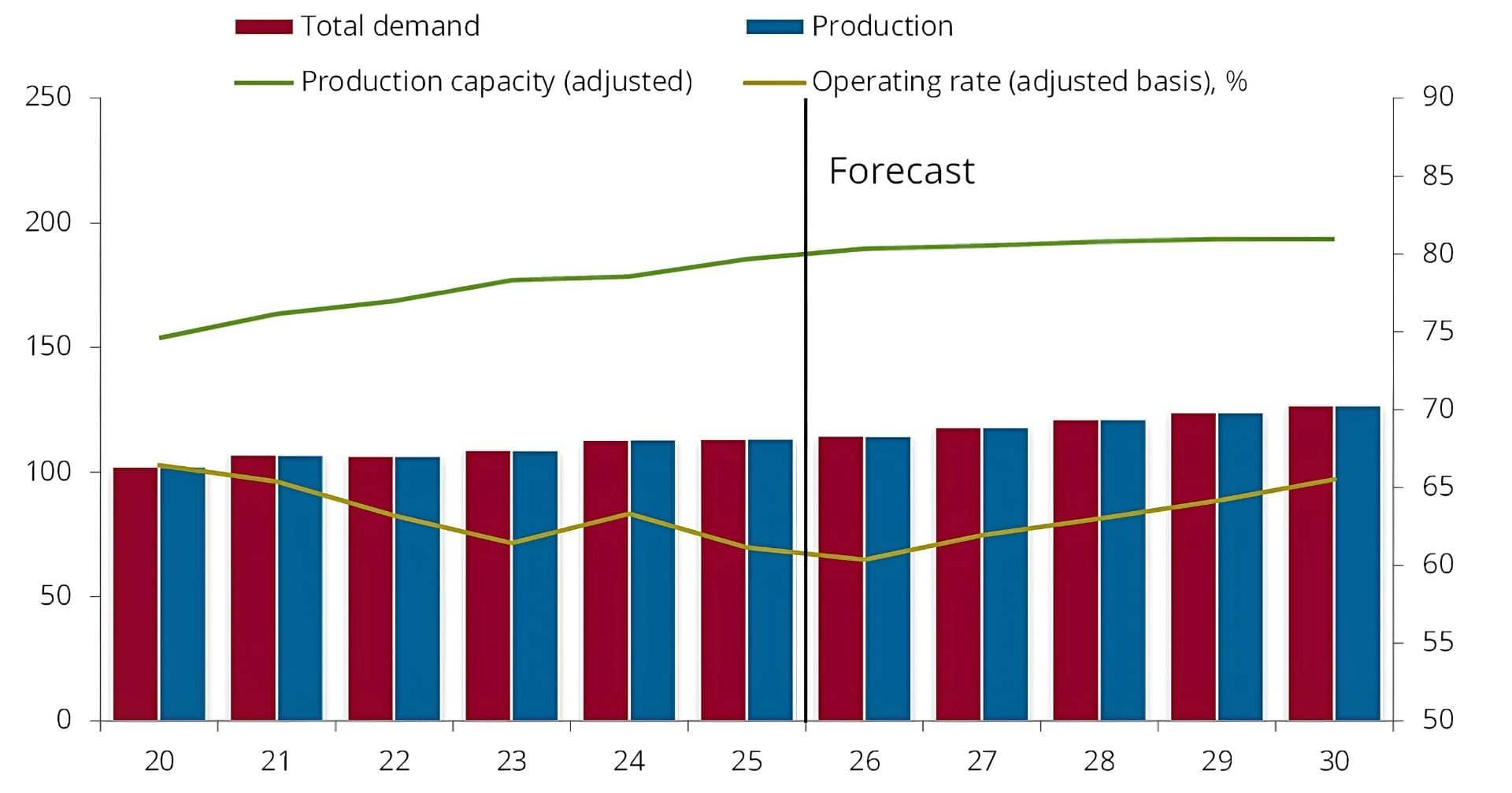

What does the outlook look like beyond 2026?

Methanol capacity expansions will slow significantly through 2030, with most additions concentrated in China, via integrated CTO, and the Middle East. We continue to expect tightening natural gas supply across major producing regions to constrain global capacity further, starting with the announced idling of Methanex’s 860 ktpa Titan unit in Trinidad and Tobago by end-Q3 26. Even so, recent Middle East developments increase the likelihood of at least one new world-scale methanol project being built by the end of the decade, with further longer-term additions expected in North America, albeit restricted by inflated construction costs. We expect previous demand trends to return by 2027 as global supply chains rebalance between Q4 26 and Q1 27, assuming Strait of Hormuz disruptions begin to ease by late Q3 26 and no significant unplanned production outages arise. Overall, our supply and demand outlook through 2030 continues to support methanol pricing moving towards sustained reinvestment levels, with any further reduction in Middle East supply likely to accelerate that pace.