Weekend effect in WTI options could be eliminated by emergence of 24/7 crude perpetuals

May 19, 2026

Key Insights

- The structural Friday IV selloff in prompt WTI options could permanently disappear as perpetual adoption grows.

- Traders can now hedge options through weekend due to 24/7 WTI perpetual futures on crypto exchanges.

- YTD notional volume has reached $65 billion, with weekends averaging roughly 30% of weekday intensity.

- There is a clear early-mover advantage for participants willing to adopt these new venues.

The dynamics of short-dated WTI options pricing are set to change due to the emergence and rapid growth of 24/7 WTI crude oil perpetual futures on crypto and spread betting exchanges. For the first time, traders can hedge options exposure through the weekend, when geopolitical risk has become disproportionately concentrated. This development has implications for the well-documented “weekend effect” in short-dated WTI options, where implied volatility is structurally depressed on Fridays as long gamma holders liquidate positions they cannot hedge over the market closure.

The structural origin of the weekend effect lies in a tension between theory and market mechanics. The Black-Scholes framework assumes variance accrues continuously and that delta hedging is always available—neither of which holds over a weekend. In practice, WTI futures trade on CME for roughly 23 hours per day on weekdays and not at all from Friday 16:00 CT to Sunday 17:00 CT. This gap creates a well-documented pattern in short-dated options pricing. Holders of long gamma positions do not want to pay theta over a weekend they cannot hedge through, so they liquidate into Friday close, depressing implied volatility. The selling pressure then dissipates on Monday open and implied volatility (IV) recovers. The net effect is a structurally positive IV move from Friday close to Monday open.

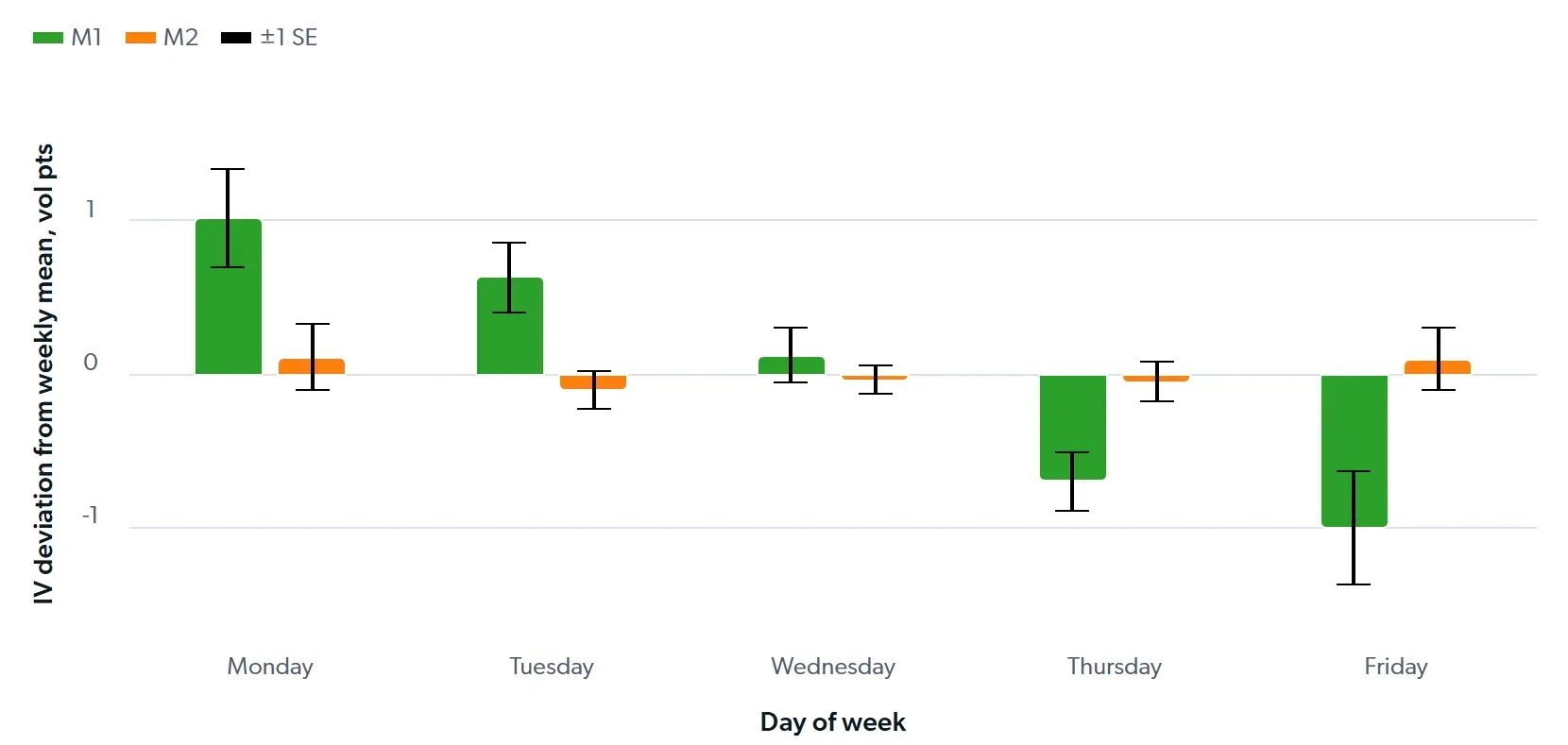

Since 2022, M1 at-the-money (ATM) IV has deviated by nearly one volatility point below its weekly mean on Fridays and recovered by a similar magnitude on Mondays, a statistically significant and persistent pattern (see Figure 1). Crucially, M2 shows almost no weekday pattern, consistent with the weekend representing a smaller fraction of remaining time value for deferred contracts and therefore less incentive to liquidate. The structural Friday IV selloff in prompt WTI options could permanently disappear as perpetual adoption grows. Traders can now hedge options through weekend due to 24/7 WTI perpetual futures on crypto exchanges. YTD notional volume has reached $65 billion, with weekends averaging roughly 30% of weekday intensity. There is a clear early-mover advantage for participants willing to adopt these new venues.

Fig 1: WTI ATM IV weekday seasonality, May 2022–May 2026

Source: Energy Aspects

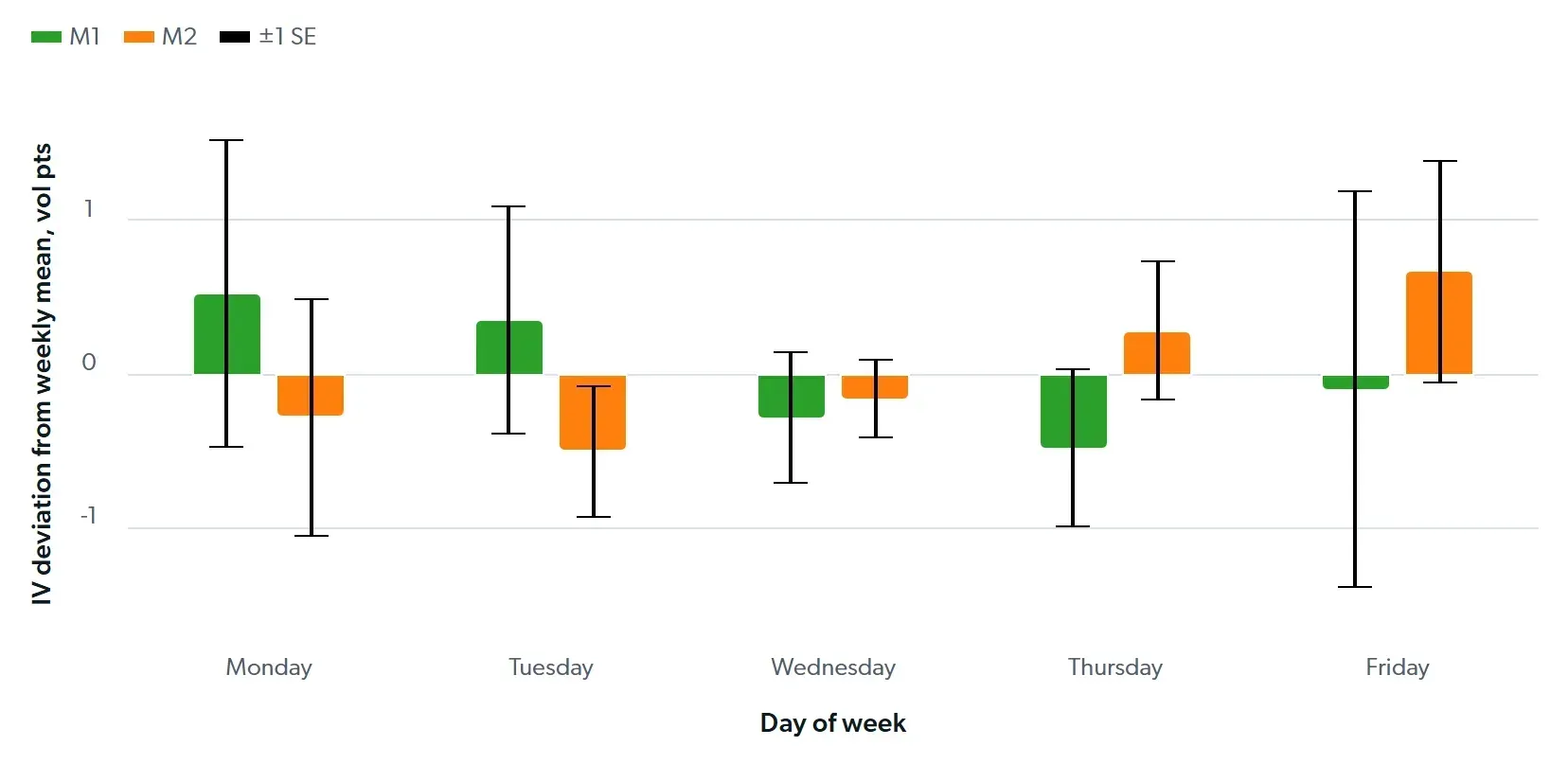

But the past 12 months tells a more nuanced story. The Friday M1 trough has largely disappeared in the recent sample while M2 is now showing a positive Friday deviation with much wider error bars (see Figure 2). However, M1 still underperforms M2 on Fridays, suggesting the weekend effect has not vanished, rather it is being offset by competing forces. We attribute this to two dynamics. First, the geopolitical environment since the US–Iran escalation has made weekends riskier. Diplomatic developments, military briefings and OPEC-related announcements have disproportionately broken over weekends when political cover is thinner. This has reduced the incentive to sell Friday gamma and, in some cases, created demand for it. Second, and more recent, the emergence of 24/7 WTI crude oil perpetual futures on crypto exchanges is beginning to change the hedging calculus, and the volume data suggest this market is maturing faster than many expected.

Fig 2: WTI ATM IV weekday seasonality, May 2025–May 2026

Source: Energy Aspects

Across WTI and Brent perpetuals, with WTI accounting for roughly 70% of flow.

Weekend days average $340M notional — sufficient to delta-hedge a moderately sized options book over a two-day window.

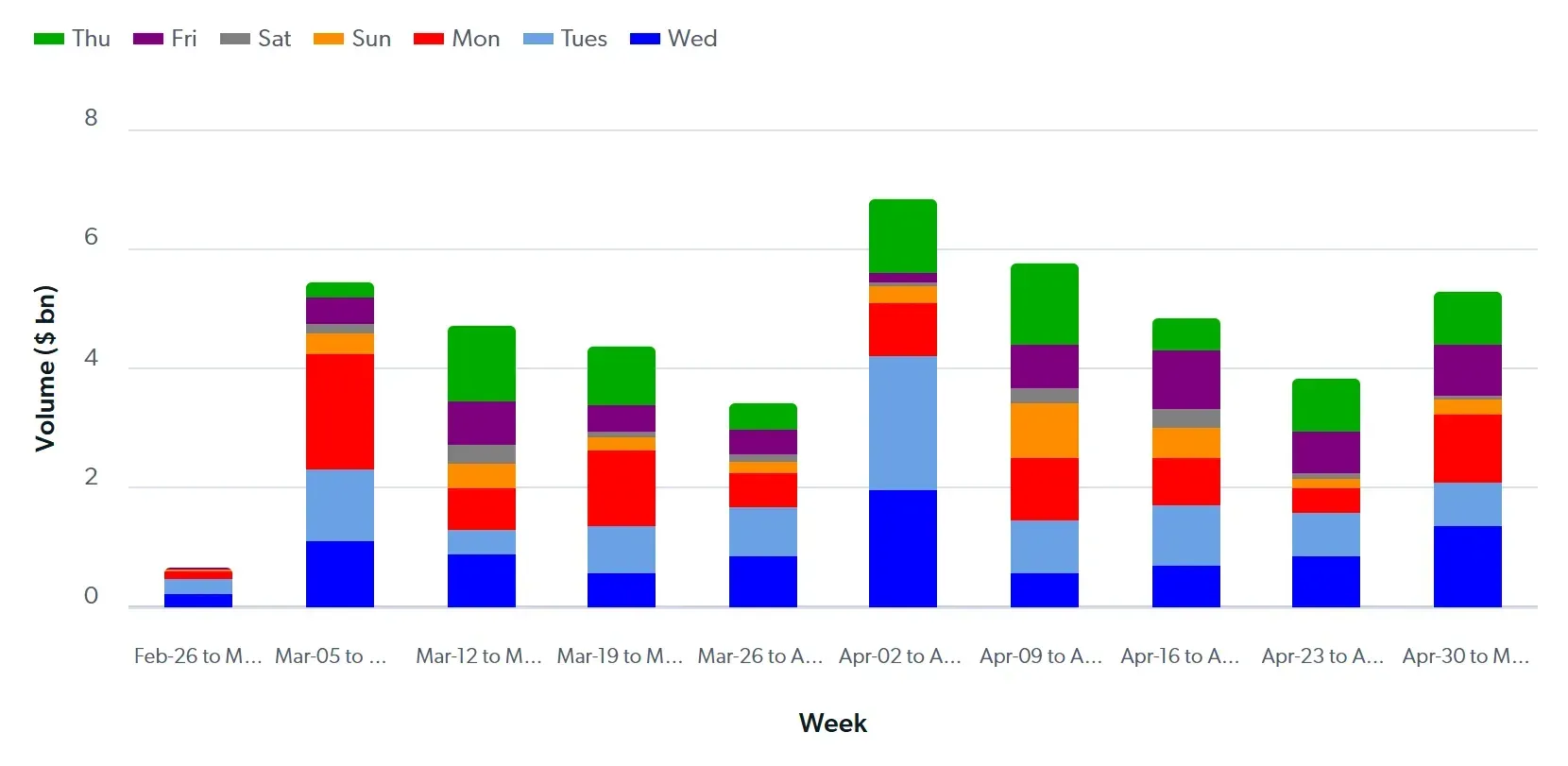

Venues, including Bullish, now offer WTI perpetual futures that trade around the clock, including weekends. Bullish offers a perpetual that indirectly references the WTI contract and has provided us with volume data. The data are instructive. YTD notional volume across WTI and Brent perpetuals has reached $65 billion, with WTI accounting for roughly 70% of flow [see Figure 3]. Average weekday volume is $1.14 billion notional while weekend days average $340 million, approximately 30% of weekday intensity. This is not NYMEX-scale liquidity but would be sufficient to delta-hedge a moderately sized options book over a two-day window.

Fig 3: WTI Volume by Week (Thu-Wed) from Feb-May 2026

Source: Energy Aspects

The growth trajectory has been steep. Daily volumes were negligible in late February at $13–25 million and ramped through March before exploding in early April. The peak day was 7 April at $3.3 billion, coinciding with Trump’s ultimatum deadline for Iran to reopen the Strait of Hormuz. Weekend volume is bumpy and event-driven, ranging from $79 million on 2–3 May, when headlines were quiet, to $1.3 billion on 12 April when US–Iran talks in Islamabad collapsed and Trump announced a naval blockade of vessels transiting Hormuz.

The perpetual’s funding rate mechanism keeps its price anchored to the underlying, if a trader priced options off the perpetual directly over the weekend then it could provide a viable hedging instrument for the duration of the market closure. When CME reopens on Monday, the perpetual converges back to the NYMEX benchmark, with any residual basis at that point representing a small second-order risk relative to the gamma P&L captured over the weekend. Cross-margining across NYMEX and a crypto venue is an operational consideration but limited in impact given the short two-day duration of the exposure.

The emergence of these perpetuals means it is now possible to buy NYMEX WTI options on Friday afternoon into the IV trough, trade the long gamma position over the weekend using the perpetual, and monetise variance that the NYMEX options market has historically priced as un-hedgeable dead time. Any gamma P&L accumulated over the weekend would be supplemented by IV recovery on Monday open. In the current geopolitical environment where weekend risk events are frequent, structurally cheap options and newly available hedging are likely to attract growing attention.

Recent Posts