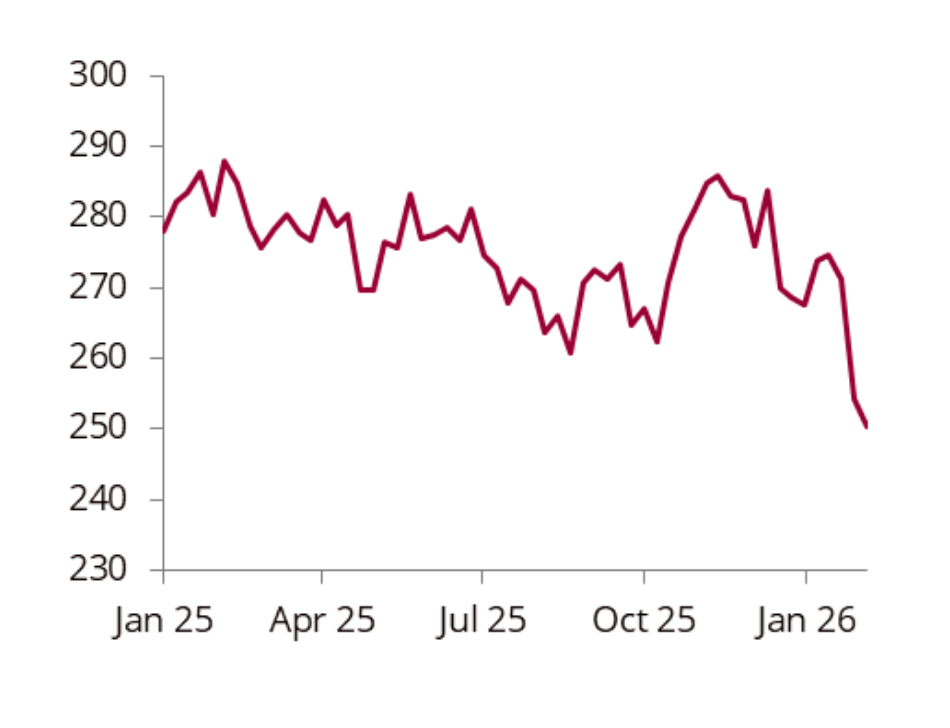

EU gas storage stands 15 bcm below the five-year average. Our analysis explains why TTF prices need to stay elevated through summer.

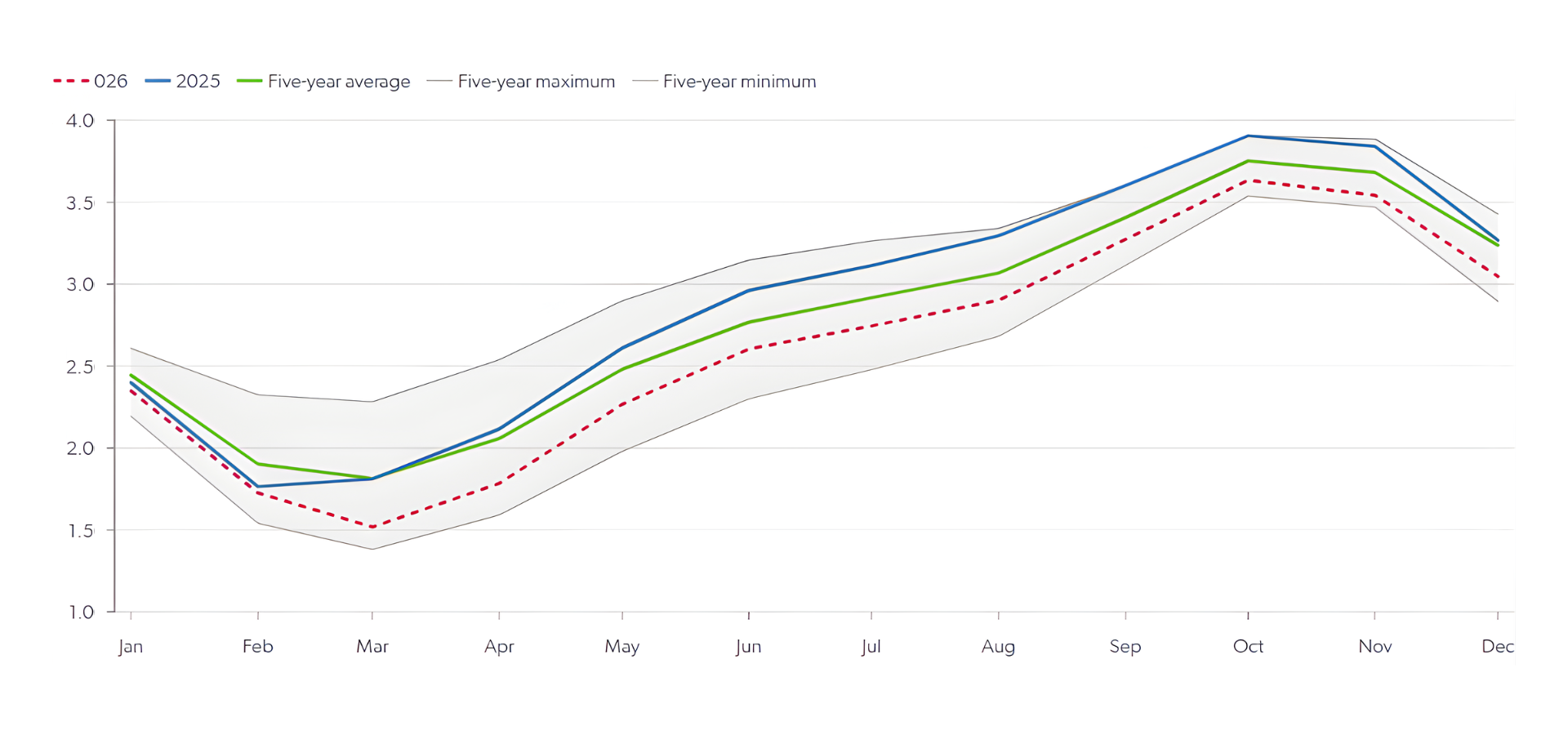

Mainstream media is already running oil glut stories for next year, built almost entirely on the assumption that China's crude demand has structurally collapsed.

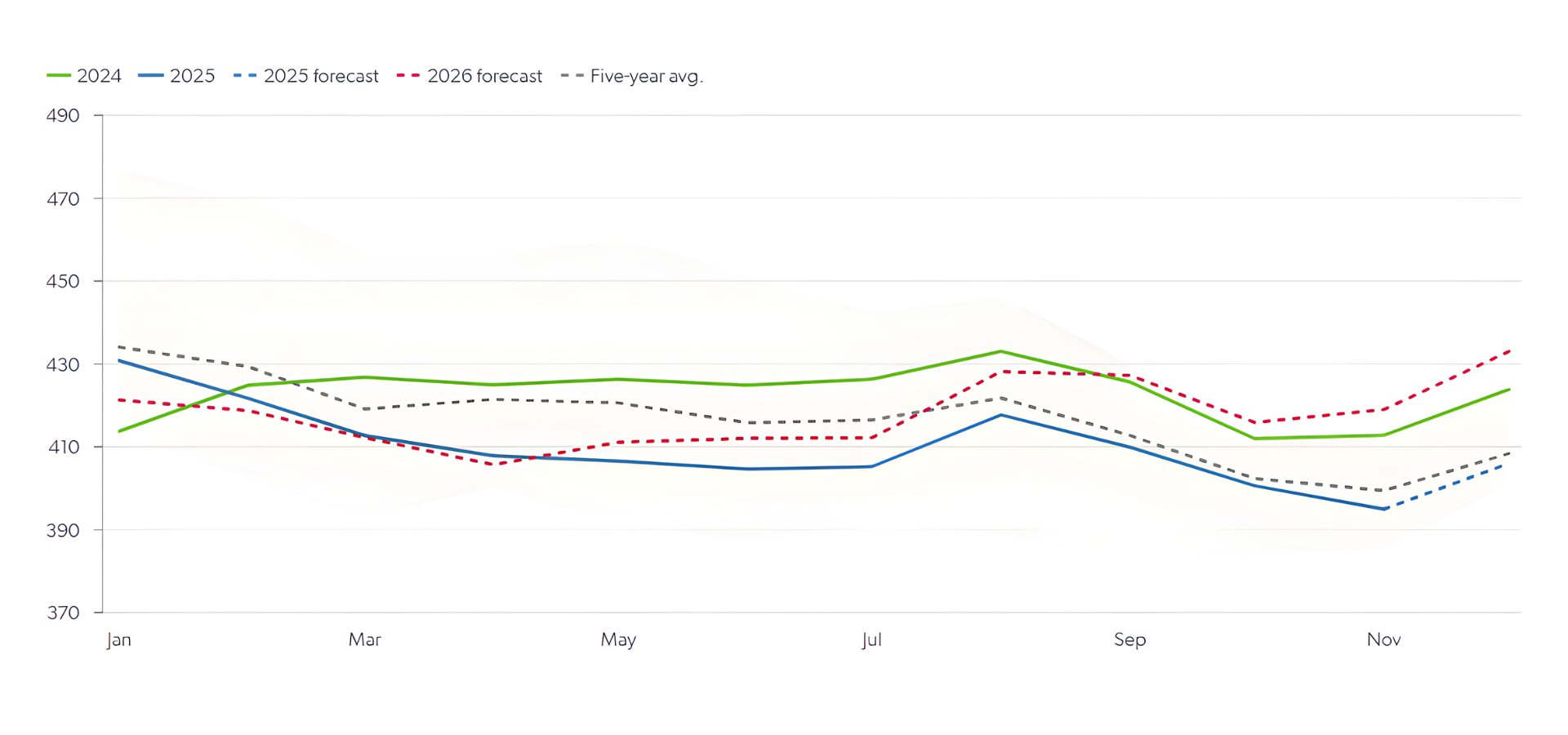

Our North America power outlook heading into summer covers PJM price strength, ERCOT large load reforms and volatile RGGI prices.