Financial flows play a critical role in market pricing across all asset classes. For traders and risk managers navigating volatile environments, understanding positioning dynamics, liquidity, and risk constraints is essential for effective decision-making. Our research applies this flow-based systematic approach across energy, metals, agriculture, and financial markets, providing crucial context that fundamental analysis alone cannot deliver.

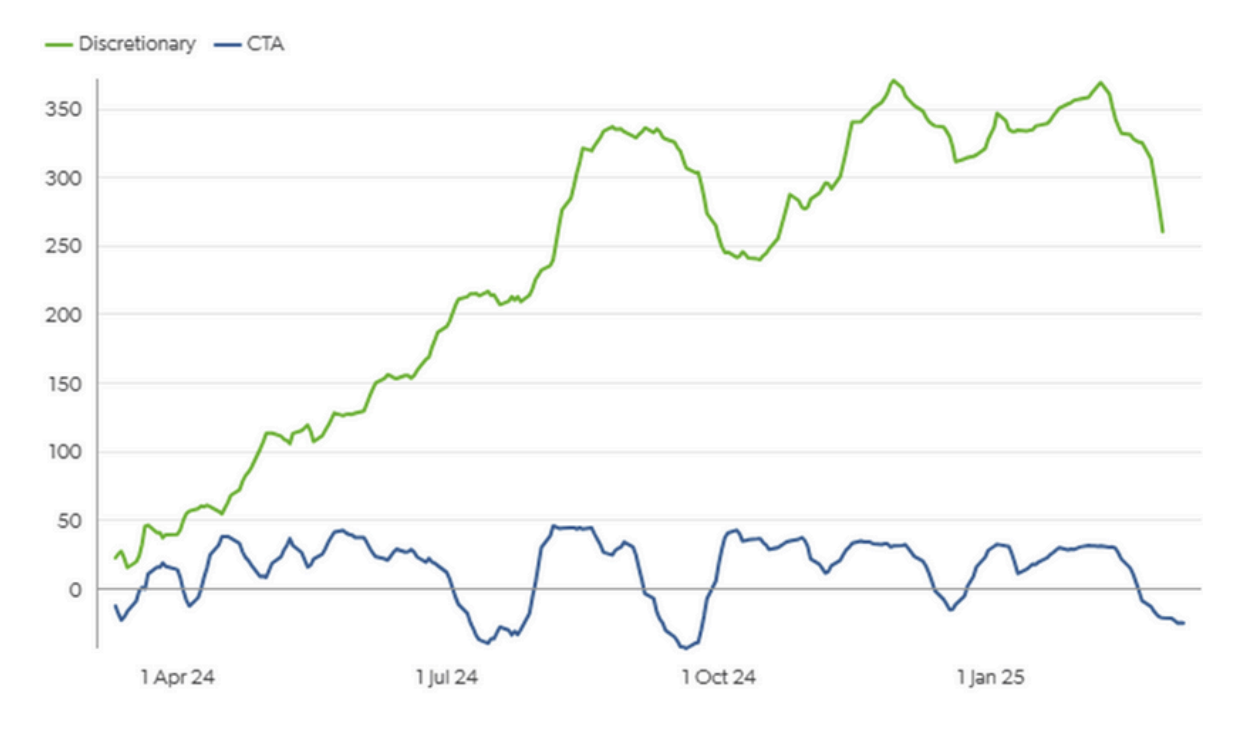

In early February 2025, discretionary fund net-long positioning in TTF peaked at a record 369k lots at €54/MWh. By March, positioning had dropped 30% to 261k lots, with prices declining to €40/MWh.

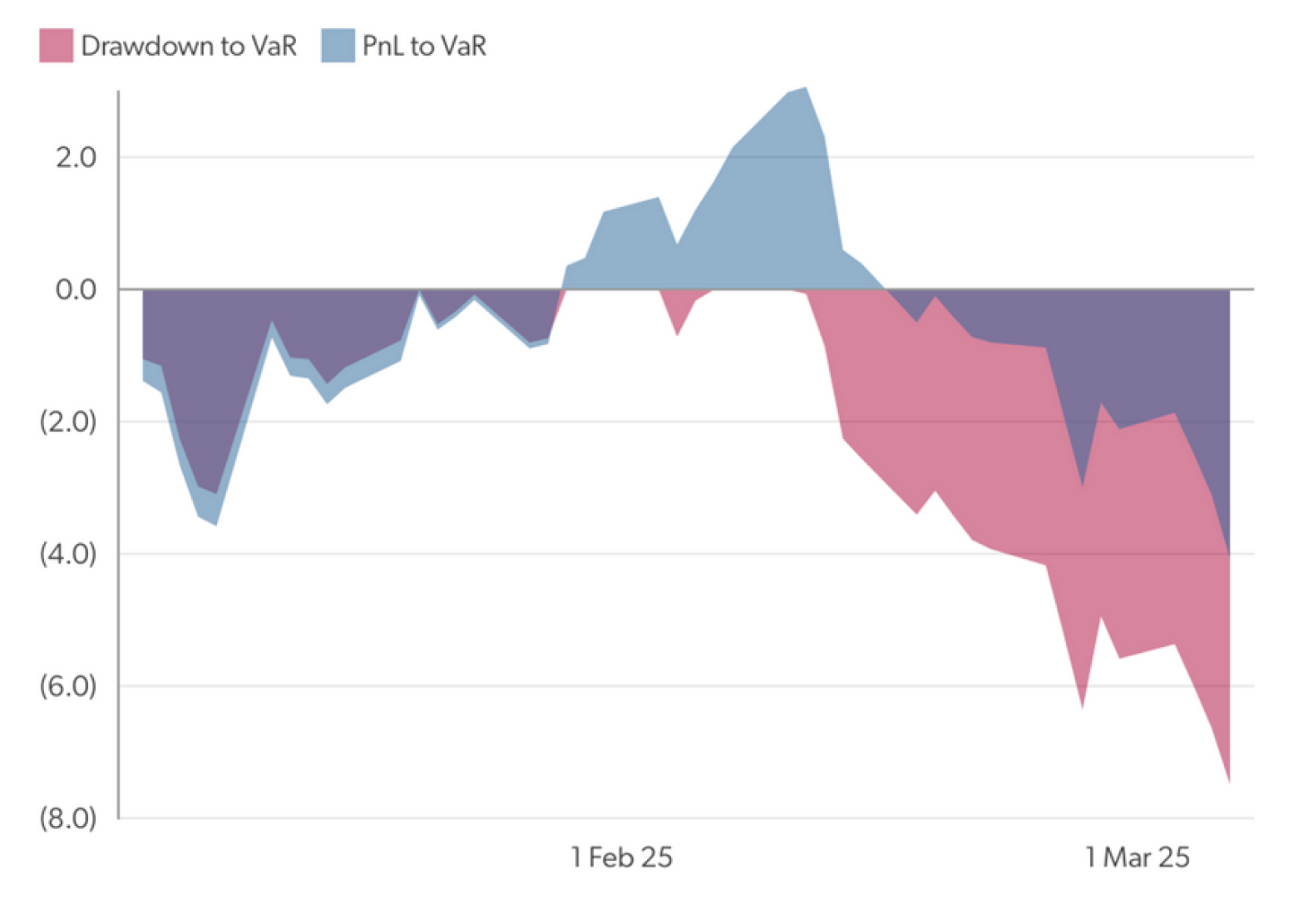

The summary below consists of excerpts from recent EA Quant research and highlights how our flow-based analysis enabled our clients to anticipate and manage risks during this significant market shift.