Your one-stop shop for real-time global energy market data and intelligence

March 6, 2026

The escalating Iran conflict is severely disrupting energy markets, especially shipping, with freight rates skyrocketing, complicating refining margins. From even before the conflict began, Energy Aspects has helped clients navigate the risks.

20th February 2026 – Geopolitical Outlook

February’s Geopolitical Outlook highlighted to EA clients that US strikes on Iran were increasingly likely, and Iran may try to disrupt Hormuz transits if it felt in an existential battle.

Read below an excerpt from the Outlook report:

Iran is no match for US firepower, but it would aim to absorb initial strikes and suck the US into a longer war of attrition using asymmetric capabilities, such as missile and drone swarms and maritime sea-denial tactics, directed by dispersed command and control. Facing a potentially existential campaign—especially if domestic protests reignite—Iran could be motivated to raise costs to the US by impeding energy transit through Hormuz. Given that threat, it is likely that any initial US campaign will include strikes against IRGC naval and short-range missile assets.

23rd February 2026 – Perspectives

In last week’s Perspectives, we reiterated that rising tensions in the Middle East were heightening risks to energy flows through the Strait of Hormuz. We noted that the US would likely seek to neutralise Iran’s naval and ballistic missile capabilities, and while this could limit prolonged disruptions, the risk of sporadic attacks on regional energy infrastructure would persist.

Read below an excerpt from the Perspectives report:

On top of this, the Middle East region is more fragile, and the vulnerability of oil volumes transiting the Strait of Hormuz cannot be entirely discounted.

Facing a potentially existential campaign—especially if domestic protests reignite—Iran could be motivated to raise costs to the US by impeding energy transit through the Strait of Hormuz. This risk is likely to lead to caution among shippers in the early days of any conflict.

Brent 25-Delta options skew

Source: Energy Aspects

The potential Iranian threat against Hormuz means that the early stages of any US campaign are likely to include a focus on neutralising IRGC naval and short-range missile assets. US early success against such targets would limit the potential for any sustained halt in regional oil and LNG transit. But the US will find it harder to eliminate any risk of one-off attacks by Iran or proxy groups, given the wide range of potential targets across the region not just disrupting transit flows alone.

27th February 2026 – EA Live (19:12)

US–Iran tensions dominate into weekend, but physical market struggling

Crude strengthened ahead of the weekend yet again with US–Iran risks driving reluctance to hold shorts, but weakening fundamentals leave the market poised for a Monday selloff if there is no Iran strike.

Today, President Trump said he was “not happy” with how Iran was negotiating, but noted “we haven’t made a final decision”. We maintain that all outcomes remain possible, and that despite new technical talks scheduled for next week, progress towards a deal that meets minimum US demands has been insufficient.

April-26 Brent expires today, with the first four windows averaging around $0.05/bbl backwardation. However, physical markets continue to weaken, and Forties sold at Dated -$0.85/bbl, the first benchmark cargo to change hands at a negative differential this year.

That’s all for this week, but we’ll post on Sunday following the OPEC8+ meeting. We expect members to agree to resume unwinding voluntary production cuts in April.

28th February 2026 – EA Live (13:11)

Broad strikes on Iran start conflict that could extend for weeks

The US and Israel have launched broad military strikes against targets across Iran, following weeks of tension as we have been warning. Early indications are these included military and regime leadership sites (reportedly including the Supreme Leader’s office) and even Kharg Island, although it is unclear at this stage whether the naval base was the target and if this will disrupt Iranian oil exports.

Qatar has temporarily suspended maritime navigation. Numerous other precautions are being taken across the region including flight diversions/cancellations.

We maintain our view that the campaign launched today will be a more sustained and significant operation than last June’s US-Israeli strikes. Over recent weeks, the US military has built up a regional presence that can sustain high-intensity operations for weeks, including refuelling aircraft that could support strike missions by well over 200 warplanes. US plans likely include scope to escalate further depending on Iran’s reaction.

- Iran is no match for US firepower but would aim to absorb initial strikes and suck the US into a longer war of attrition using asymmetric capabilities.

- We maintain Iran could be motivated to impede energy transit through the Strait of Hormuz as it is likely to view this as an existential crisis.

- Iran has already launched retaliatory missile attacks on Israel and US bases in neighbouring countries such as the UAE, Qatar, Iraq and Kuwait.

Our next post will focus in more depth on the initial energy market risks and impacts of the conflict.

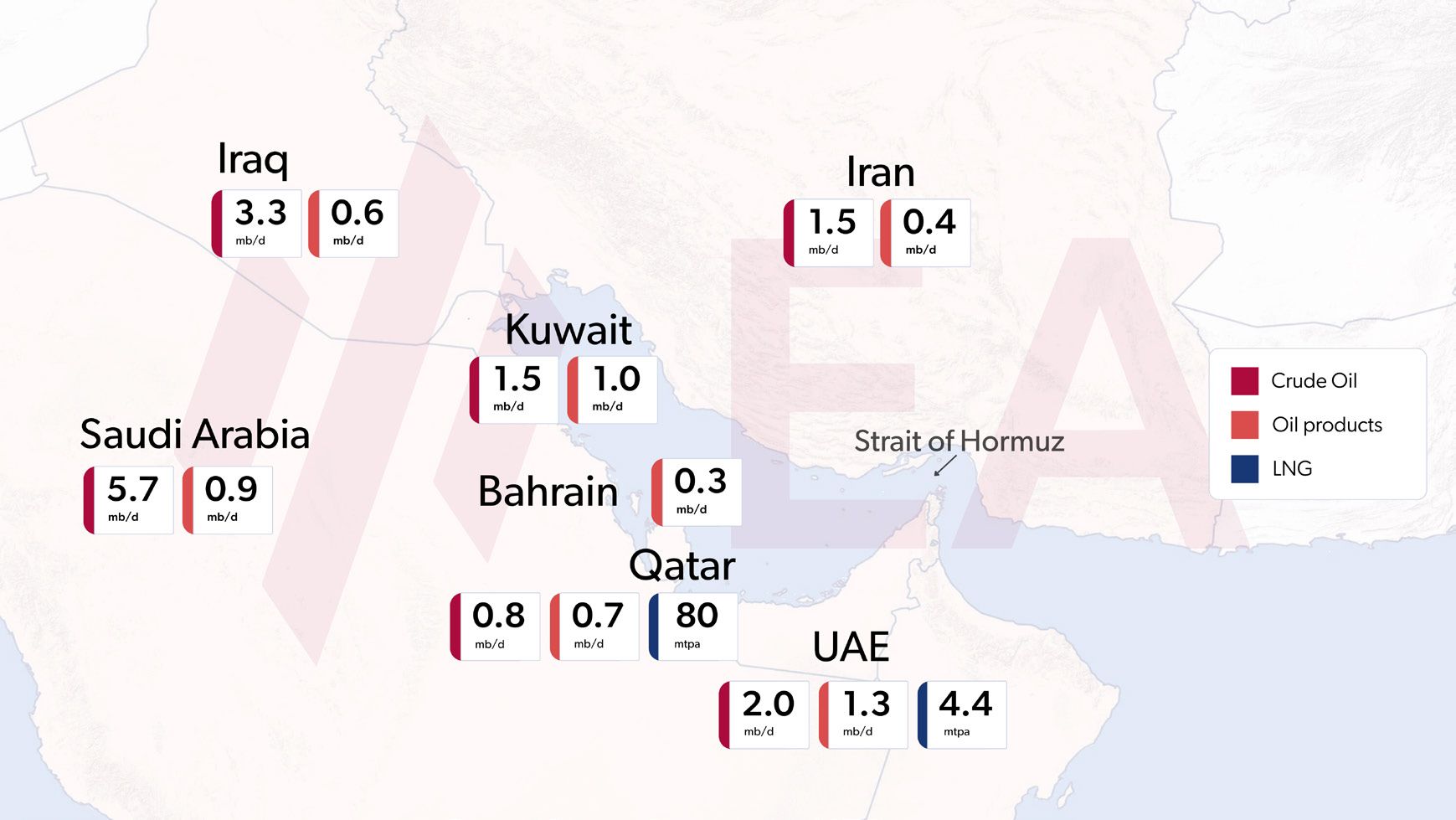

Strait of Hormuz oil, products and LNG flows, indicative export volumes by country, 2025 avg

Note: Indicative, rounded volumes. Oil products include LPG. Excludes non-seaborne exports.

Source: OilX, LNG Cargo Tracking, Energy Aspects

28th February 2026 – EA Live (14:13)

Assessment of initial energy market impacts from Iran conflict

Here is our assessment of the initial energy-related impacts of the conflict as of 2 p.m. GMT on 28 February:

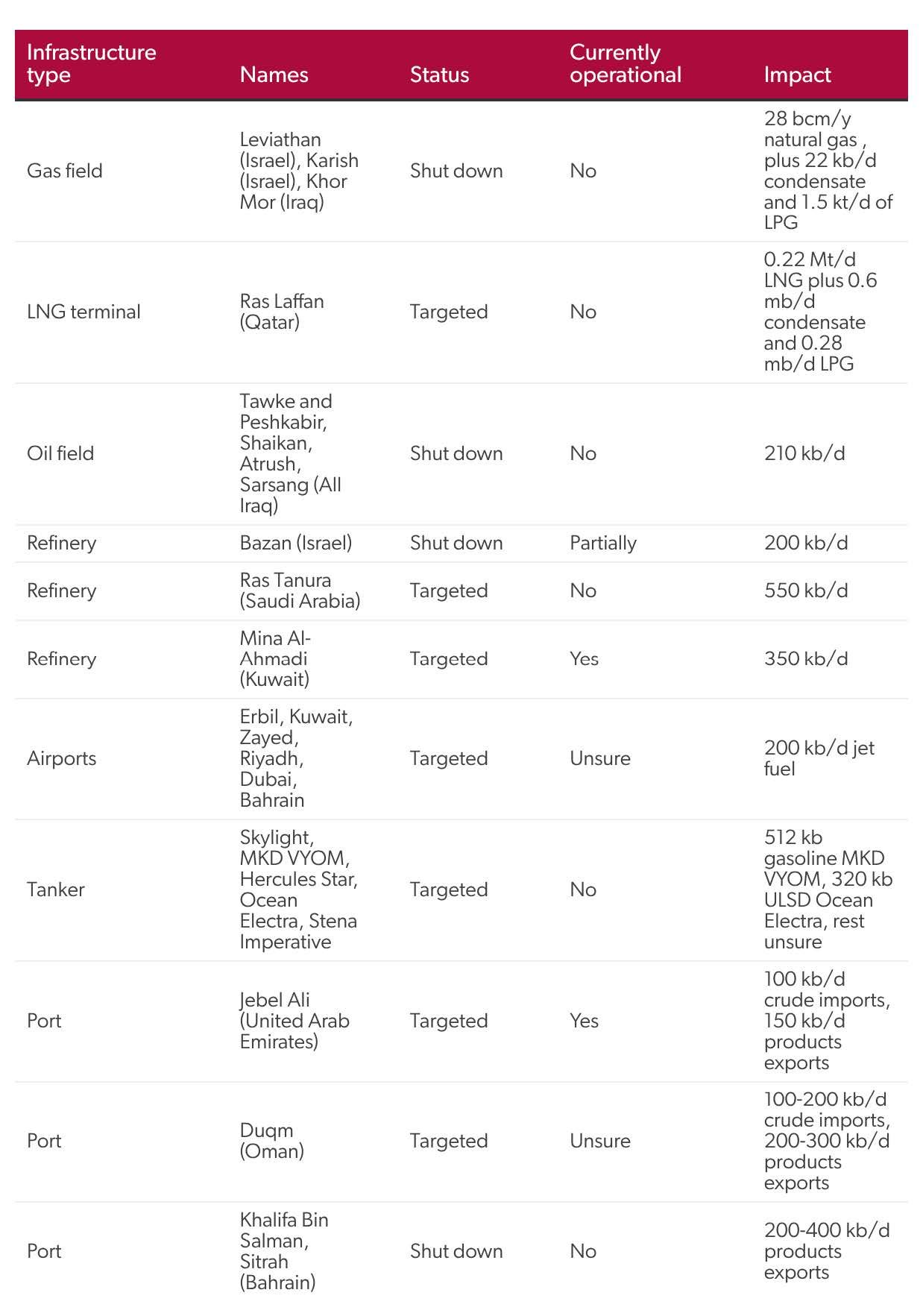

- No reports of strikes on oil and gas fields or refineries across the Middle East so far. Israel has ordered precautionary shutdowns of the 12 bcm/y Leviathan and 8 bcm/y Karish gas fields, and the 0.20 mb/d Bazian refinery.

- We have not yet seen any indications that an explosion on Kharg Island, reported in local media, will affect Iranian oil exports. We will provide a full assessment tomorrow once more satellite imagery is available.

- Some shippers are halting oil and LNG tanker transits through the Strait of Hormuz for at least the next few days, while other vessels continue moving for now. Extensive AIS spoofing and GPS jamming likely during the conflict.

- The Houthis have announced plans to immediately resume maritime attacks in the Red Sea, which is likely to increase war risk premiums.

- OPEC8+ meets tomorrow and will seek to reassure the oil market. We expect the group will announce larger target increase for April (0.41–0.55 mb/d) than we previously anticipated as a precaution. Saudi Arabia may also confirm its contingency plans are already in effect.

1st March 2026 – EA Live (13:40)

Iran conflict in intense phase, extending shipper caution through Hormuz

The Iranian conflict remains in an intense phase, with US and Israeli strikes on Iran continuing and Iran firing missiles and drone barrages at targets across the region. Tankers and other vessels have increasingly halted transits through the Strait of Hormuz. UKMTO has so far today (1 March) reported incidents that appear to involve IRGC attacks on two vessels, although these have not officially been confirmed yet (more on this later). These attacks are likely to strengthen and extend shipper caution, increasing the disruption to energy trade flows.

Meanwhile, Iran named a transitional council to project leadership continuity despite the killing of Supreme Leader Khamenei. There are no clear signs of fracturing within Iran’s military leadership or evidence that reported losses among the IRGC’s high command have significantly degraded Iran’s ability or willingness to respond militarily.

Both the US and Israel have said strikes will continue for at least several more days. Alongside strikes on Iran’s retaliatory capacity, Israel has shifted aerial operations to intense sorties against regime targets inside Tehran.

1st March 2026 – EA Live (18:58)

Gas prices to rally on Iran conflict; JKM-TTF should widen

Gas prices will likely rally at the open today as the Iran conflict is disrupting some LNG flows through the Strait of Hormuz. CTA flows could exacerbate TTF price moves, as mean strategy distance to flipping is at zero according to our Quant team.

Together Qatar and UAE typically export more than 7 Mt/m of LNG via Hormuz (20% of global supply). About 85% of these volumes have flowed to Asia in recent months. As such, the JKM may rise more than the TTF initially, widening JKM–TTF spreads.

Israel has temporarily halted production at the 12 bcm/y Leviathan and 8 bcm/y Karish gas fields, and has stopped pipeline supplies to Egypt (0.9 bcm/month). Egypt could fuel-switch to fuel oil and curtail industry. The country also has capacity to raise spot LNG imports by up to 1 bcm in March but may not be willing to pay premiums. An interruption to Turkish pipeline gas imports from Iran (0.5 bcm/month) could also increase LNG demand.

Europe has little buffer to withstand a prolonged pull from Asia on Atlantic basin alternatives. Disruptions to Italy and Poland’s contractual deliveries from Qatar pose some upside to regional basis prices.

2nd March 2026 – EA Live (08:51)

Upside for oil prices as attacks on Middle East energy assets reported

Oil prices jumped at the open and have further upside from current levels as the market responds to the conflict in the Middle East.

Late yesterday (1 March), President Donald Trump indicated the US military campaign could last for up to four weeks. Earlier this morning, senior Iranian official Ali Larijani rejected negotiations with the US. Diplomatic efforts will continue, and events can shift quickly. But the chances of a swift resolution that avoids supply disruptions has fallen. Accordingly, Asia is likely to buy alternative crudes rather than remain on the sidelines, driving freight higher.

The direct impact on energy fundamentals is also growing. Strait of Hormuz flows have declined sharply, with four tankers attacked to date. Energy infrastructure is also sustaining damage. Saudi Arabia’s 0.55 mb/d Ras Tanura refinery was struck by an Iranian drone this morning, and unconfirmed reports indicate damage to refineries in Kuwait and Iran. We will provide further updates throughout the day.

2nd March 2026 – EA Live (10:56)

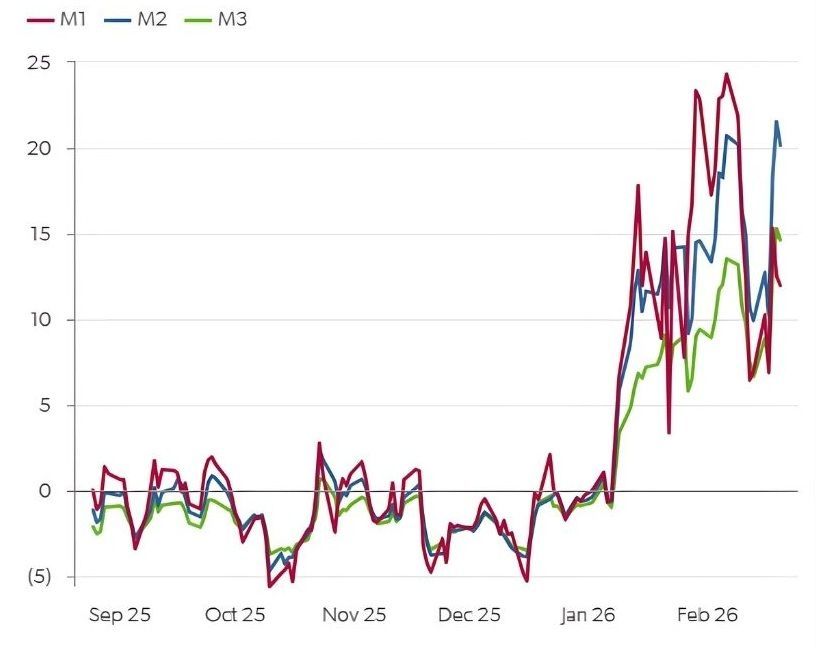

Crude options flows muted by uncertainty

The volatility response in crude options this morning has been surprisingly muted given

the elevated positioning. This is partly explained by the already extreme levels of volatility and skew, which we have reported on previously.

The volatility response has almost exactly tracked the skew expectations for near-the-money options, which indicates that flows so far are light and there is no sign yet of either profit-taking on long call positions or panic covering of shorts.

Brent M1 25-day skew, %

Source: Energy Aspects

On the gamma front, the reaction has been more painful for our dealer portfolio. Daily at-the-money breakevens sat at approximately $2.75/bbl on Friday (27 February). Since the close, the price path has extended beyond $21/bbl, far more than the breakeven expectations. Actual P&L implications for this depend on the performance of the trader (or algorithm) executing the hedging, but it is likely to have been an uncomfortable ride.

2nd March 2026 – EA Live (17:37)

Qatar condensate, NGLs and GTL output curtailed by Ras Laffan halt

Ras Laffan suspended LNG production prior to today’s drone attack due to ongoing maritime disruptions inside the Strait of Hormuz, primarily driven by limited storage capacity to maintain liquefaction rates. Qatar’s condensate production, averaging around 0.75 mb/d, is highly centralised at Ras Laffan and is largely linked to LNG trains for export, with current LNG-linked output estimated at 0.6 mb/d.

Gas processing plant (GPP) capacity in the Ras Laffan area adds a further 0.15 mb/d of condensate, of which 30–50 kb/d is used domestically. We expect condensate production could fall to around 0.1 mb/d, while Ras Laffan LNG operations are suspended, as some GPP volumes enter storage. LPG production, which is entirely exported, may drop by 0.28 mb/d.

Ras Laffan refinery operates two condensate splitters, each with 0.15 mb/d capacity, producing 0.13 mb/d naphtha, 85 kb/d jet and 54 kb/d diesel—risking naphtha and middle distillate exports. Oryx 32 kb/d GTL facility will also likely cease operations.

2nd March 2026 – EA Live (19:20)

US–Iran conflict: Impacted energy infrastructure

Drone and missile strikes across the Middle East are impacting energy infrastructure, but so far confirmed outages have been limited. Port infrastructure handling a total of 2.3 mb/d of liquids flow has been targeted, but latest information suggests minimal disruption. The risk to shipping is more evident, with five tankers confirmed hit so far and several operators suspending Hormuz transits entirely, although this is in part due to AIS jamming. Several oil fields in Iraqi Kurdistan have been precautionarily shut, with a combined production loss of 0.2 mb/d, reducing flows to the Ceyhan terminal in Turkey. Fields in Southern Iraq may also have to shut production if Basrah loadings have to slow or stop as ships are unable to traverse the Strait of Hormuz.

Qatar’s condensate production could fall by 0.6 mb/d and LPG by 0.28 mb/d due to the Ras Laffan LNG shutdown.

Impacted Middle East energy infrastructure

Note: Shut down is precautionary closure

Source: Energy Aspects

Recent Posts