What are the risks to the linkage timeline?

The most prominent near-term risk is UK domestic politics. Uncertainty around Keir Starmer's tenure as prime minister has weighed on UKA prices in recent months. Energy Aspects had lowered its Q2 2026 UKA price forecast by £1/t on this political risk. A leadership challenge could delay the summit, though our view is that even a change of Labour leader would not derail linkage, given broad cross-party support for closer EU integration.

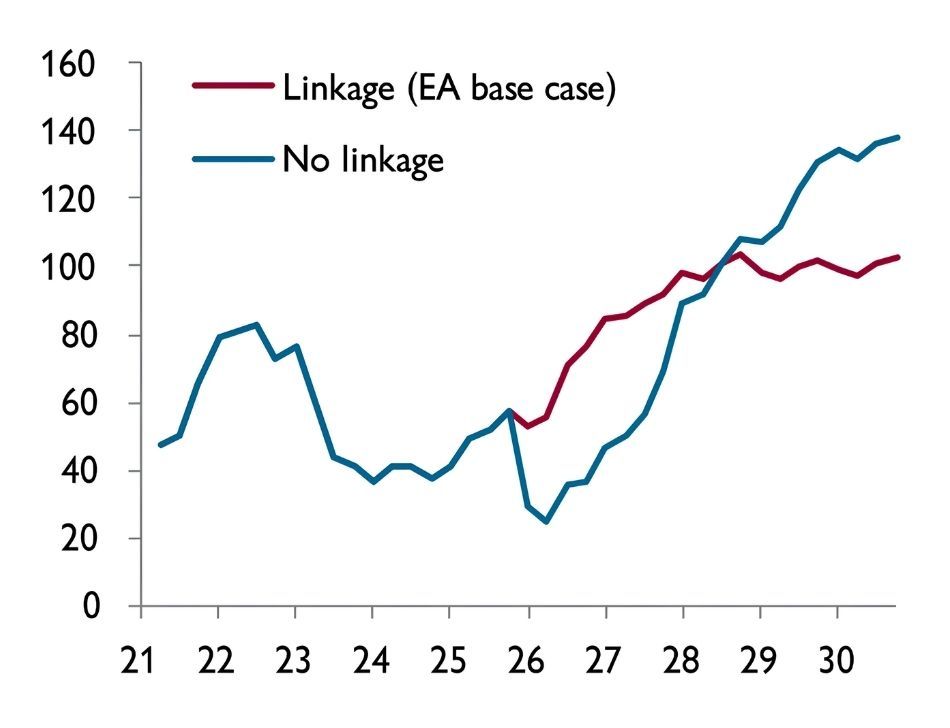

If the summit is pushed back to end-2026, we forecast UKA prices to average £57/t in H2 2026, versus £71/t in the base case. A complete breakdown in talks, which we consider unlikely, would see UKA prices fall to around £32/t by year-end. Linkage negotiations are part of a broader package that includes agreements on food standards and a youth mobility scheme, adding complexity to the timeline.

How does EU ETS reform change the picture?

The European Commission is due to publish EU ETS reform proposals in July, coinciding with the summit. Our post-reform risk case lowers the average EUA price over 2026-30 by €7/t, reflecting plausible rule changes including adjustments to the Market Stability Reserve, slower CBAM phase-in and the frontloading of Industrial Decarbonisation Bank financing. The reform process adds almost 400 Mt of supply over 2026-30 in the risk case.

For carbon market participants, the interaction between linkage and reform is critical. If EU ETS reforms loosen balances more than expected, the convergence target for UKA prices shifts lower. Conversely, if reforms are modest, the combined market would be tighter, supporting prices across both systems. The sequencing of reform proposals and linkage confirmation in July makes the month a pivotal one for European carbon pricing.

What does this mean for UK emitters and compliance buyers?

UK ETS fundamentals will have a limited role on prices as long as linkage remains the key pricing nexus. UK verified emissions came in at 80 Mt in 2025, down 6 Mt year on year, with industrial closures in steel, refining and chemicals driving the decline. The scrapping of the UK Carbon Price Support from April 2028 will moderately raise UKA demand in winter hours, but EA does not expect this to materially change the price outlook under a linkage scenario.

For compliance buyers, the practical implication is that hedging strategies should increasingly reference EUA price levels rather than treating the UK ETS as an isolated market. The transition period between announcement and full implementation will create opportunities for spread trading, but the direction of convergence is clear.