Liquidity is likely to remain thin over the coming weeks, and prices may drift lower unless major geopolitical outages disrupt the market. Ukraine peace talks are a major volatility driver. We think an imminent deal is unlikely, but the window for one has opened.

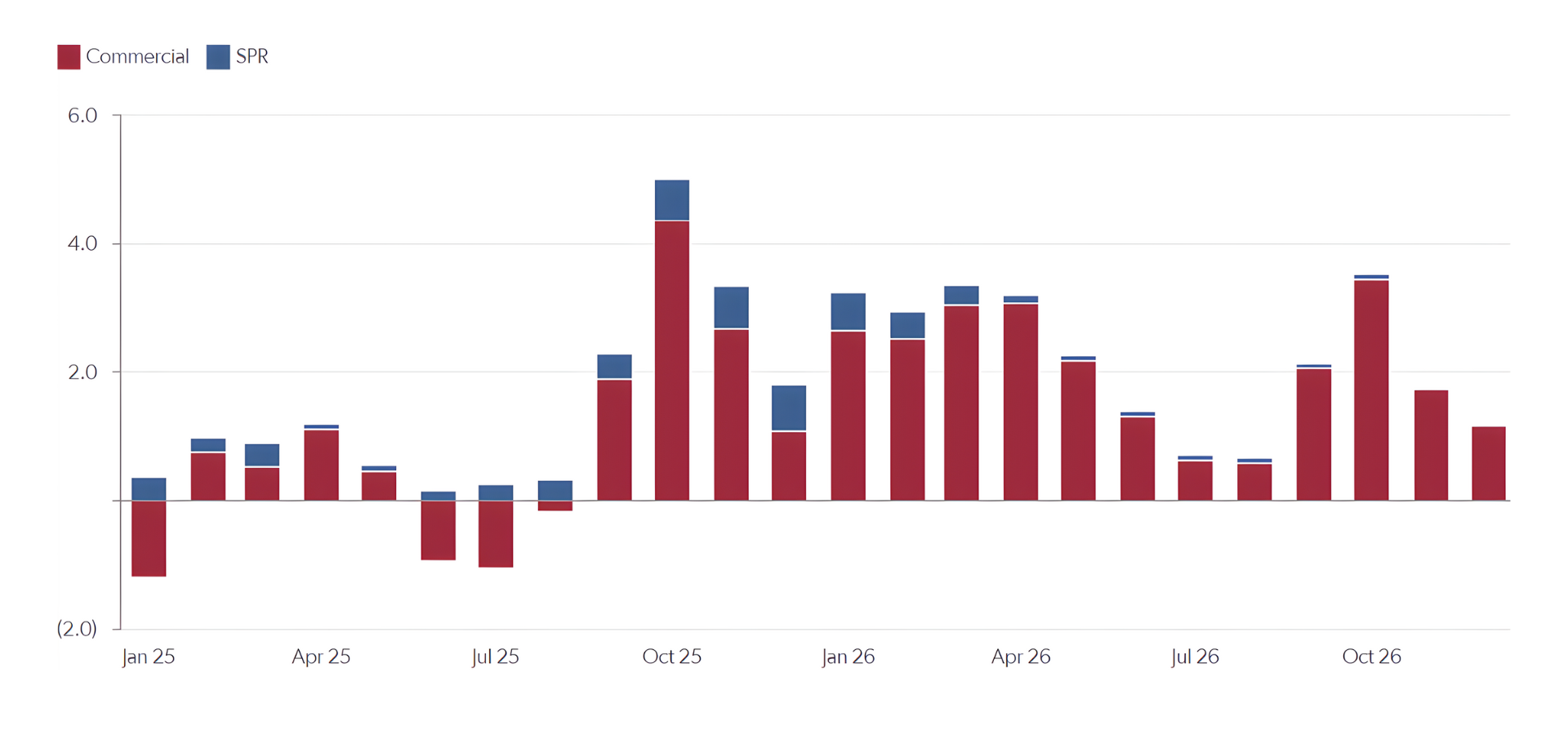

Chinese SPR buying has provided support for prices this year, and another buying round is possible in 2026, with few capacity constraints. Overall, global demand fears likely peaked in Q2 25 after “Liberation Day”, when US President Donald Trump’s tariff threats briefly unsettled markets. We forecast global liquids demand to rise by 1.2 mb/d y/y in 2026, up from 0.8 mb/d growth in 2025, despite ongoing macro and policy uncertainty.

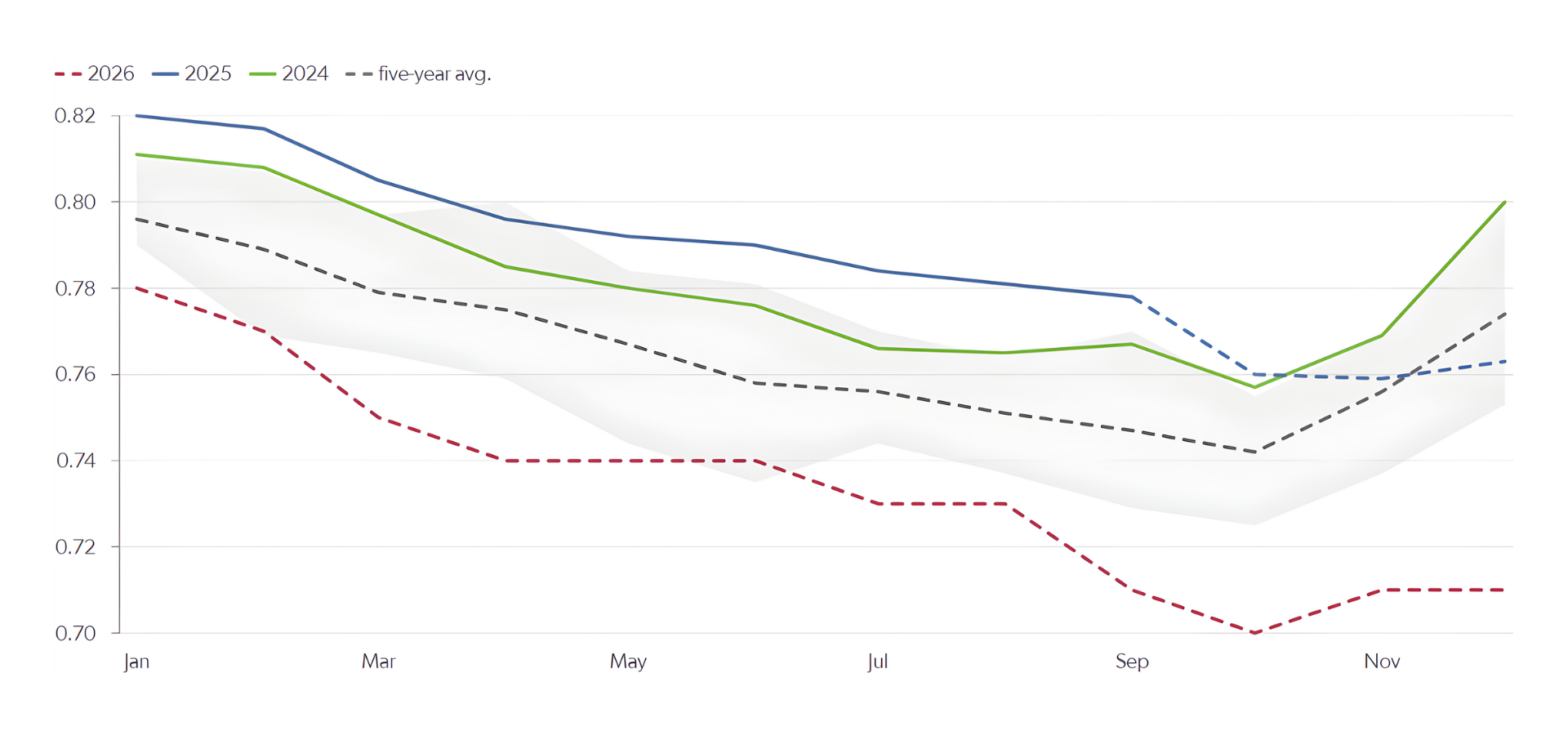

Global non-OPEC crude production is set to grow by 0.84 mb/d in 2026, but this outlook is highly price-sensitive. If Brent prices drop into the $50s for more than six months, we expect a y/y decline of 0.8 mb/d in H2 26, led by the US. OPEC+ will also play a key role in 2026—if the group continues to draw down spare capacity, it will support prices further out on the curve.