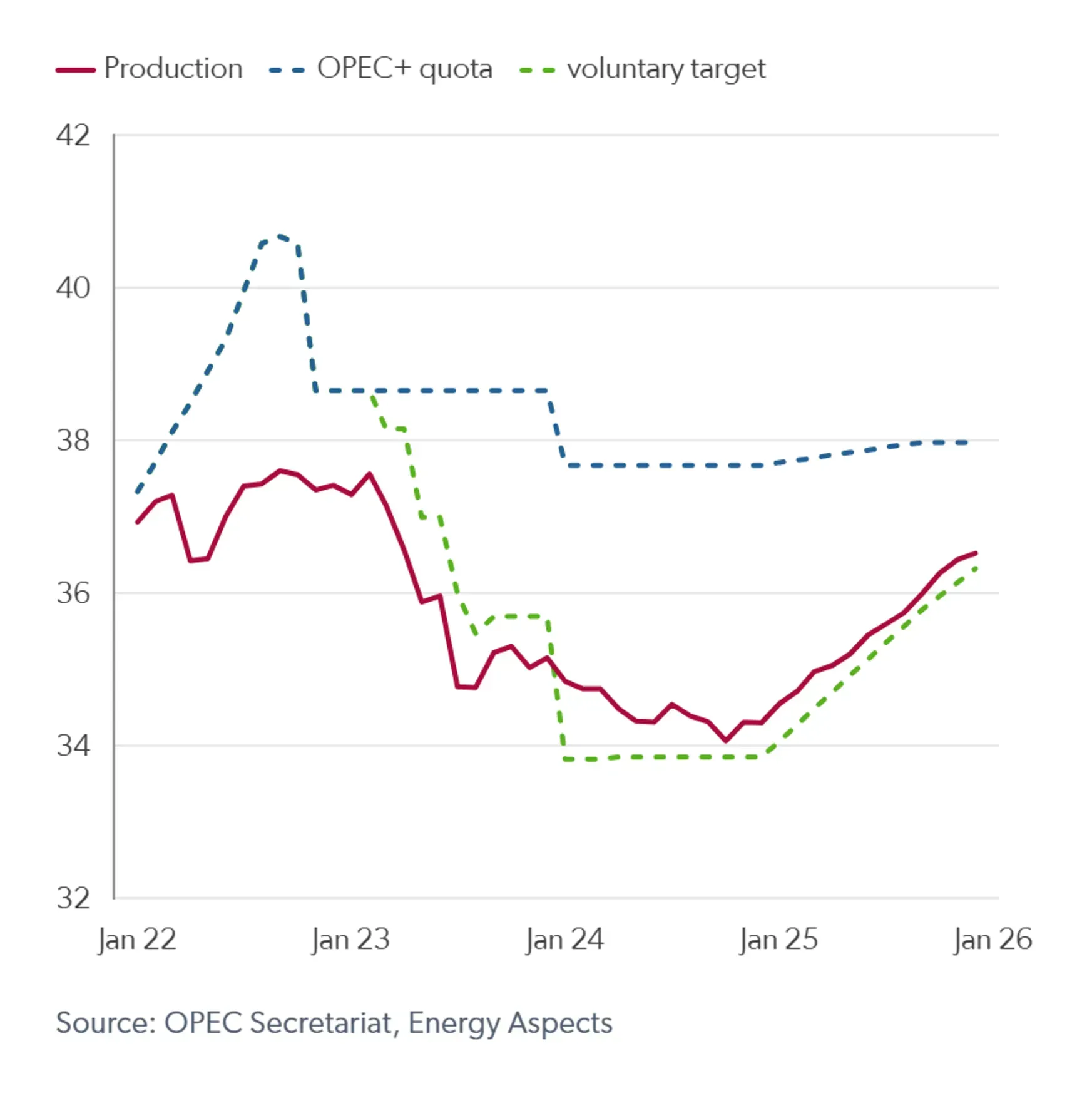

We expect tomorrow’s OPEC+ meeting (5 December) to delay the unwind of the voluntary production cut through peak refinery maintenance—most likely by three months—as the group will not want to add barrels during seasonal crude builds. Saudi energy minister Prince Abdulaziz bin Salman has long maintained that the group wants to ensure inventories remain below the five-year average. The group is likely to remain reactive and cautious given the numerous uncertainties about how the incoming Donald Trump administration in the US will impact oil markets. Our current balances assume the group unwinds the cuts from January and a three-month delay, for instance, would reduce our commercial crude builds from 0.6 mb/d to 0.1 mb/d. A delay of four or more months would remove these builds entirely.

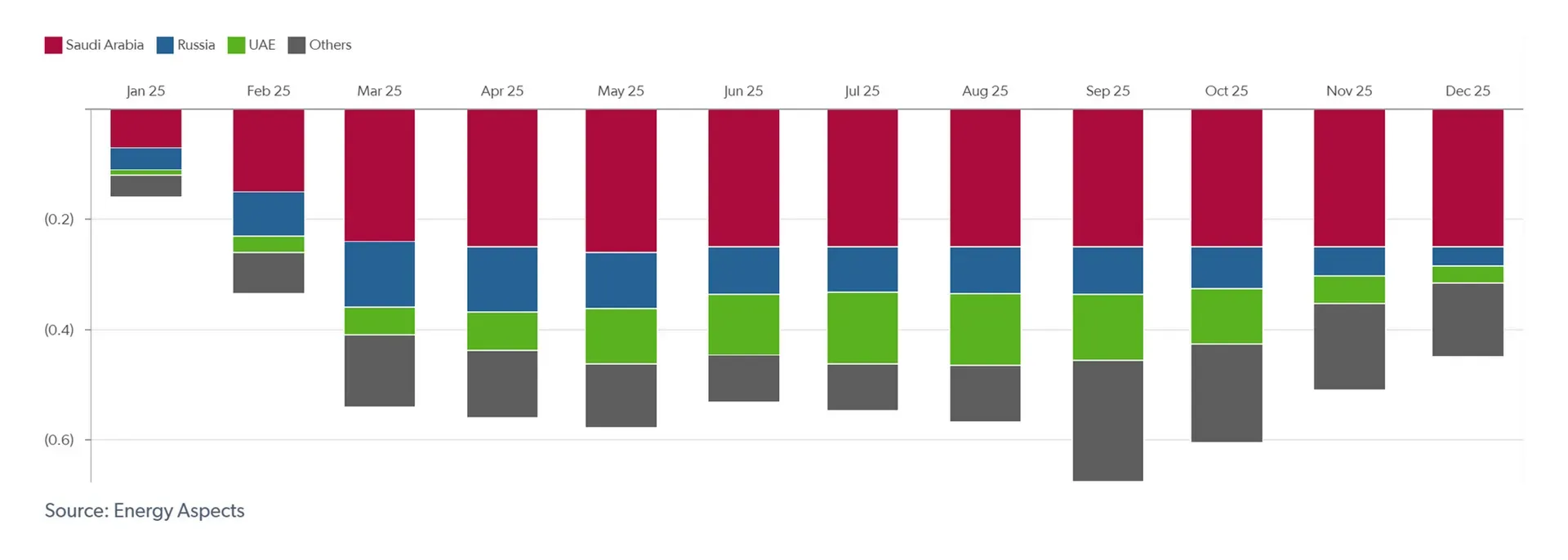

Decisions about the schedule for unwinding the 2.2 mb/d of additional voluntary cuts are taken by the eight countries participating in those cuts. The only item that would need to be agreed by all OPEC+ ministers is any change to the plans for the UAE production quota, which is currently set to gradually rise by 0.3 mb/d over January–September 2025. We believe this may get pushed back to align it with the delayed start to unwinding voluntary cuts, although this is not yet certain.

We understand the group may also consider a four- or six-month delay—and there has been market chatter suggesting the delay could be as long as 12 months. The argument for such a move would be to deliver a bullish surprise, but this would reduce the optionality to make further adjustments during H1 25, as the trajectory for inventories and Trump’s policies become clearer. In particular, we think Saudi Arabia will want to see a clear physical impact from any Trump policies before supporting OPEC+ policy changes. As such, we think the group will opt for a delay of three months to retain more flexibility next year.